Bridgewater’s Alpha-Beta Framework: How Risk Parity and Portable Alpha Generate Returns

The mechanics behind systematic macro’s most influential strategies — and their structural failure modes.

This is a detailed research piece. If you find value in institutional-quality hedge fund analysis, support this work on Patreon.

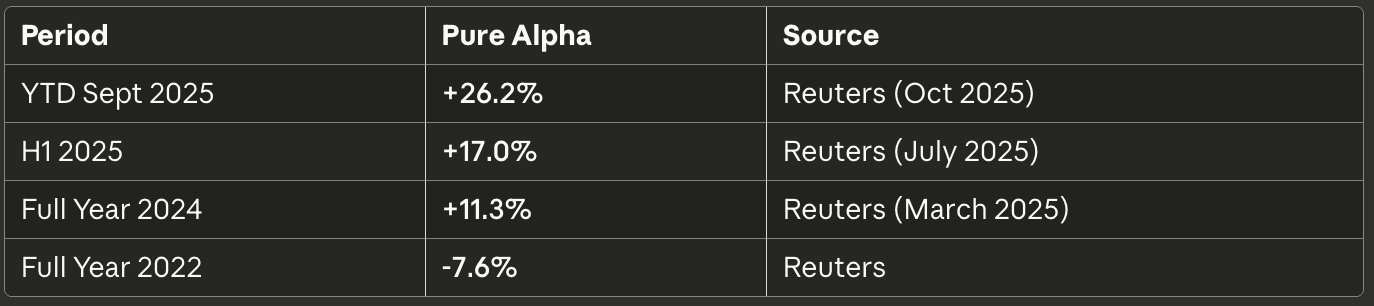

Bridgewater Associates pioneered two frameworks that reshaped institutional portfolio construction: alpha-beta separation (1990) and risk parity (1996). Pure Alpha returned +26.2% YTD through September 2025; All Weather posted +15.3% over the same period. Understanding the P&L mechanics reveals principles applicable across systematic macro.

The Core Insight: Risk Allocation ≠ Dollar Allocation

Traditional 60/40 portfolios concentrate ~90% of risk in equities. Stocks exhibit 4–5x more volatility than bonds — the 40% bond allocation barely moves the needle on portfolio risk.

Bridgewater’s solution: allocate by risk contribution, not dollars. This requires levering low-volatility assets (bonds) to equalize their risk contribution with high-volatility assets (equities).

Strategy 1: All Weather (Risk Parity Beta)

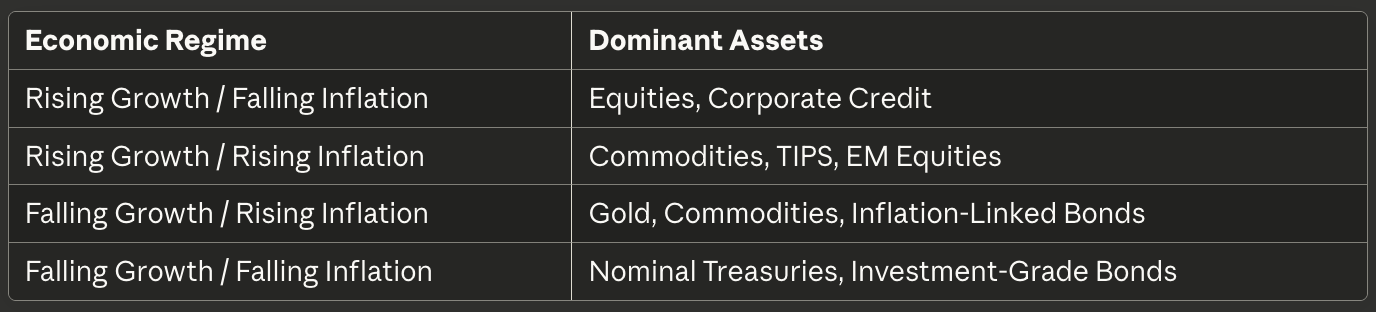

The Four-Quadrant Framework

All Weather equalizes risk across four economic environments:

No forecasting required. Weights adjust dynamically based on rolling volatility estimates — typically trailing 12-month standard deviation.

Implementation & Leverage

Unlevered risk parity allocates ~47% to bonds, ~19% to equities, and ~34% to commodities by dollar weight. To achieve 10% target volatility (matching traditional 60/40 risk), managers apply 1.5–2.0x leverage via futures, bringing notional exposure to 150–200%.

Instruments:

Equity beta: S&P 500, MSCI World futures

Bond beta: Treasury futures (2Y, 10Y, 30Y), TIPS

Commodity beta: Bloomberg Commodity Index futures, gold

The Leverage Aversion Premium

Risk parity harvests a structural mispricing: most institutional mandates prohibit leverage, forcing capital into high-volatility assets. This bids up equities relative to bonds, creating superior risk-adjusted returns for investors willing to lever low-volatility assets.

2022: When Correlation Breaks the Strategy

All Weather lost 22% in 2022 — its worst drawdown on record. The failure mechanism:

Normal regime: Growth falls → stocks drop → rates cut → bonds rise. Portfolio stable.

2022 stagflation: Inflation rises → rates hiked aggressively → both stocks and bonds drop simultaneously.

Leverage amplifies: With 2x bond exposure, the losses compounded.

Stock-bond correlation spiked to approximately +0.65 in 2022 versus the long-run average of -0.20. The diversification thesis collapsed precisely when it was needed most.

Strategy 2: Pure Alpha (Portable Alpha)

Structure

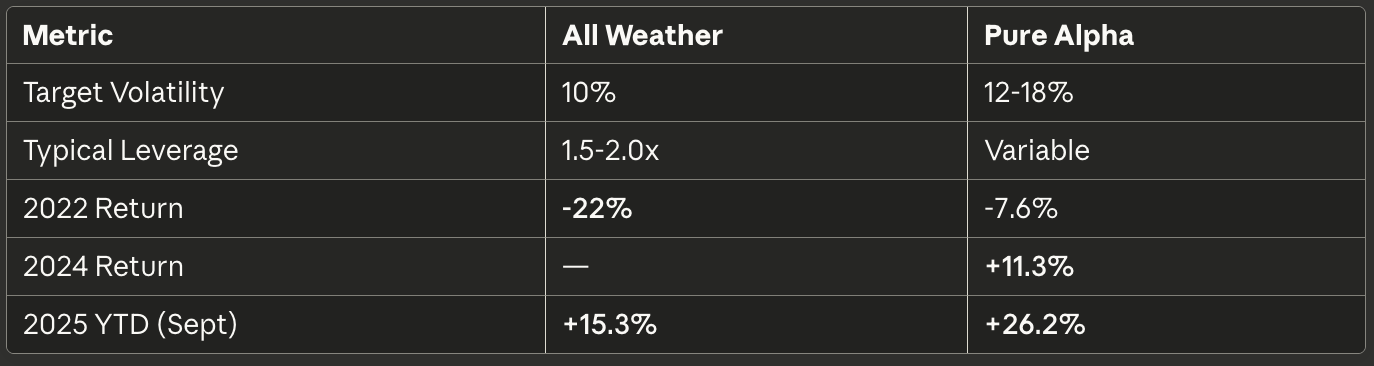

Pure Alpha runs 30–40 uncorrelated positions across bonds, currencies, equities, and commodities. Target volatility: 12% (Pure Alpha I) or 18% (Pure Alpha II).

Key characteristics:

Global macro: discretionary + systematic hybrid

Alpha overlay capability: active positions layered on client benchmarks

Designed for zero beta to traditional markets

The “Economic Machine” Framework

Bridgewater codifies cause-and-effect relationships into hundreds of “decision rules.” Positions express views on where economies sit within three cycles:

Short-term debt cycle (5–8 years): Credit expansion/contraction

Long-term debt cycle (75–100 years): Secular deleveraging

Productivity growth: Structural economic trends

Portable Alpha Implementation

Institutional investors use Pure Alpha as an overlay:

Beta exposure: Gain S&P 500 via futures (~5% margin requirement)

Alpha deployment: Remaining 95% cash allocated to Pure Alpha

Result: S&P 500 return + Pure Alpha return on the same capital base

This structure explains why capacity matters — alpha is zero-sum.

Verified Performance

The 2025 outperformance came from macro volatility driven by U.S. trade policy uncertainty — exactly the dislocated environment where discretionary macro thrives.

AUM & Capacity Management

Bridgewater deliberately shrank assets to preserve alpha:

Source: Reuters regulatory filing coverage, March 2025

The firm returned capital to clients and limited new inflows. Per Reuters: management’s goal is “to be the best, not the biggest.”

Structural Risks

Risk Parity Vulnerabilities

Correlation regime dependence: The strategy is effectively short correlation volatility. When stock-bond correlation spikes positive, the diversification thesis fails.

Leverage amplification: 2x notional = 2x losses when hedges fail.

Rising rate environments: Bonds (the largest allocation) suffer sustained drawdowns. 2022–2023 proved catastrophic for leveraged duration.

Pure Alpha Vulnerabilities

Capacity constraints: Alpha decays as AUM grows. Large positions move markets.

Framework risk: The “economic machine” reflects specific macro assumptions. Regime changes (e.g., post-2020 monetary policy) may invalidate historical relationships.

Key person transition: Leadership shifted to co-CIOs Karen Karniol-Tambour, Greg Jensen, and Bob Prince. Ray Dalio sold remaining stake in 2025.

Key Metrics Summary

Quant Takeaway

Risk parity is not passive — it’s a short correlation volatility position. Allocating to risk parity means betting the historical negative stock-bond correlation persists. This worked for 40 years of declining rates. Forward-looking, the thesis is less certain.

Pure Alpha demonstrates that alpha-beta separation allows institutions to source uncorrelated returns while maintaining benchmark exposure via derivatives. The portable alpha concept — gaining beta through futures, deploying cash to alpha strategies — remains underutilized outside top-tier allocators.

Verified Sources (Working Links)

Reuters — “Bridgewater’s flagship macro fund Pure Alpha jumps 8.1% in Q3” (Oct 2025) https://www.reuters.com/markets/us/bridgewaters-flagship-macro-fund-pure-alpha-jumps-81-outperforming-market-2025-10-01/

Reuters — “Bridgewater’s flagship Pure Alpha gains 17% in H1” (July 2025) https://www.reuters.com/markets/us/bridgewaters-flagship-pure-alpha-gains-17-h1-source-says-2025-07-01/

Reuters — “Hedge fund Bridgewater’s assets down to $92.1 billion in 2024” (March 2025) https://www.reuters.com/business/finance/hedge-fund-bridgewaters-assets-down-921-billion-2024-2025-03-31/

CAIA Association — “Risk Parity Not Performing? Blame the Weather” (Jan 2024) https://caia.org/blog/2024/01/02/risk-parity-not-performing-blame-weather

Bridgewater Associates — “The All Weather Strategy” (Official) https://www.bridgewater.com/research-and-insights/the-all-weather-strategy

State Street Global Advisors — SPDR Bridgewater All Weather ETF (ALLW) https://www.ssga.com/us/en/intermediary/capabilities/alternatives/all-weather-etf

ETF.com — “All Weather ETF Inspired by Ray Dalio Strategy Debuts” (March 2025) https://www.etf.com/sections/news/all-weather-etf-inspired-ray-dalio-strategy-debuts

Bridgewater Associates — Karen Karniol-Tambour (Co-CIO) https://www.bridgewater.com/people/karen-karniol-tambour

Markov Processes International — Risk Parity Analysis (Dec 2024) https://www.markovprocesses.com/blog/risk-parity-not-performing-blame-the-weather/

Institutional Investor — “Bridgewater Extends Strong Run” (Oct 2025) https://www.institutionalinvestor.com/article/bridgewater-extends-strong-run-gains-across-flagship-and-china-funds

📊 Support this research: https://www.patreon.com/c/NavnoorBawa

Such a fantastic post. I worked with Bridgewater in a past life. Very interesting place.