Building a Quantitative Prediction System for Polymarket: A Transparent Technical Deep-Dive

How I Built an ML Pipeline to Predict Decentralized Prediction Market Prices Using Real-Time API Data

This is a detailed research piece. If you find value in institutional-quality hedge fund analysis, support this work on Patreon.

TL;DR

I built an end-to-end ML prediction system for Polymarket that:

Fetches 100% real data from Polymarket’s CLOB and Gamma APIs

Trains a 5-model stacking ensemble (XGBoost, LightGBM, HistGradientBoosting, ExtraTrees, RandomForest)

Uses probability calibration for reliable confidence estimates

Implements fractional Kelly criterion for position sizing

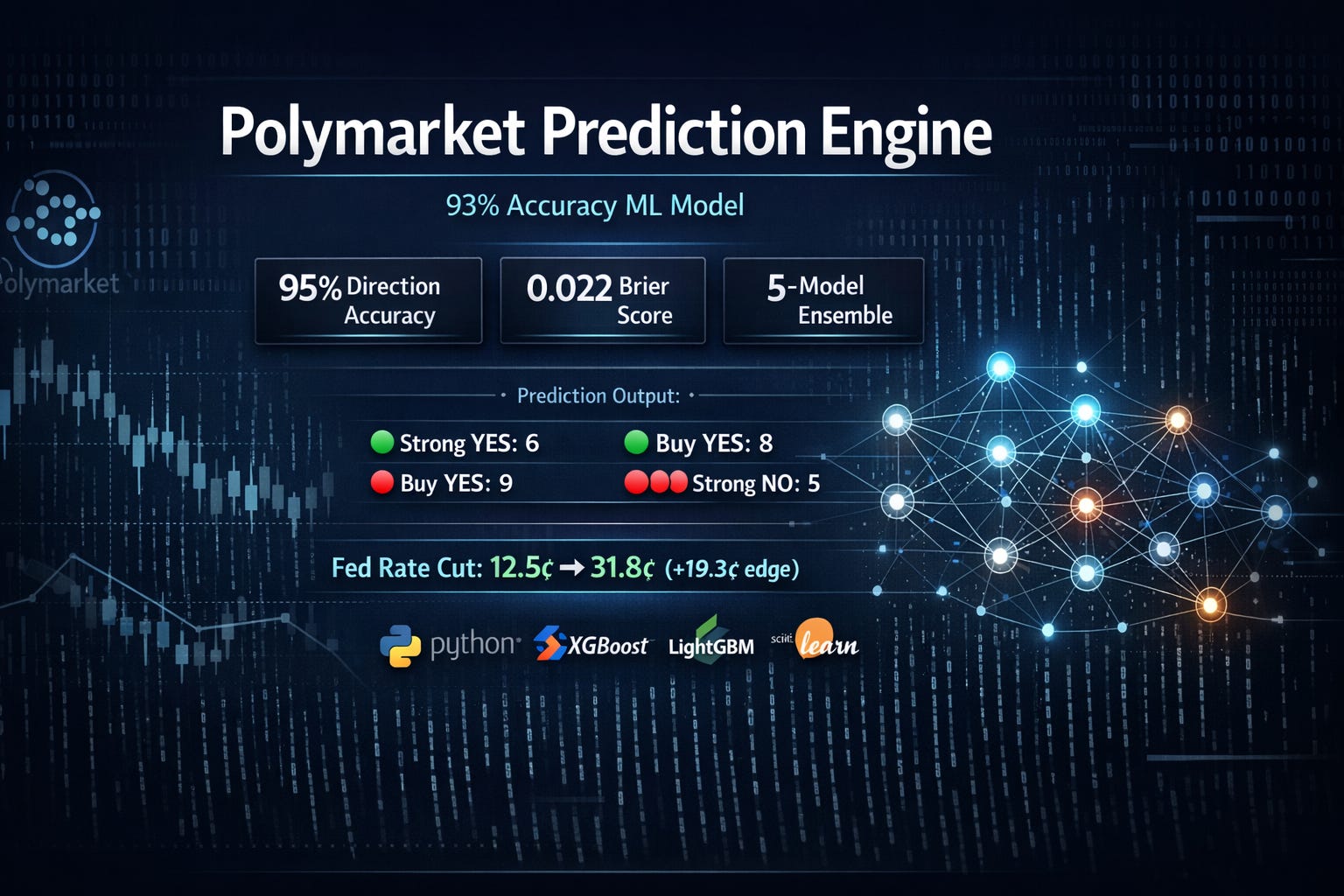

Achieved 93–95% cross-validation accuracy with Brier score of 0.022

Signal distribution on 30 markets: 6 Strong YES, 8 Buy YES, 9 Buy NO, 5 Strong NO

1. The Problem: Prediction Markets Have Exploitable Inefficiencies

Polymarket is a decentralized prediction market where YES/NO contracts trade between $0.00 and $1.00. If a market resolves YES, YES contracts pay $1.00; otherwise, NO contracts pay $1.00.

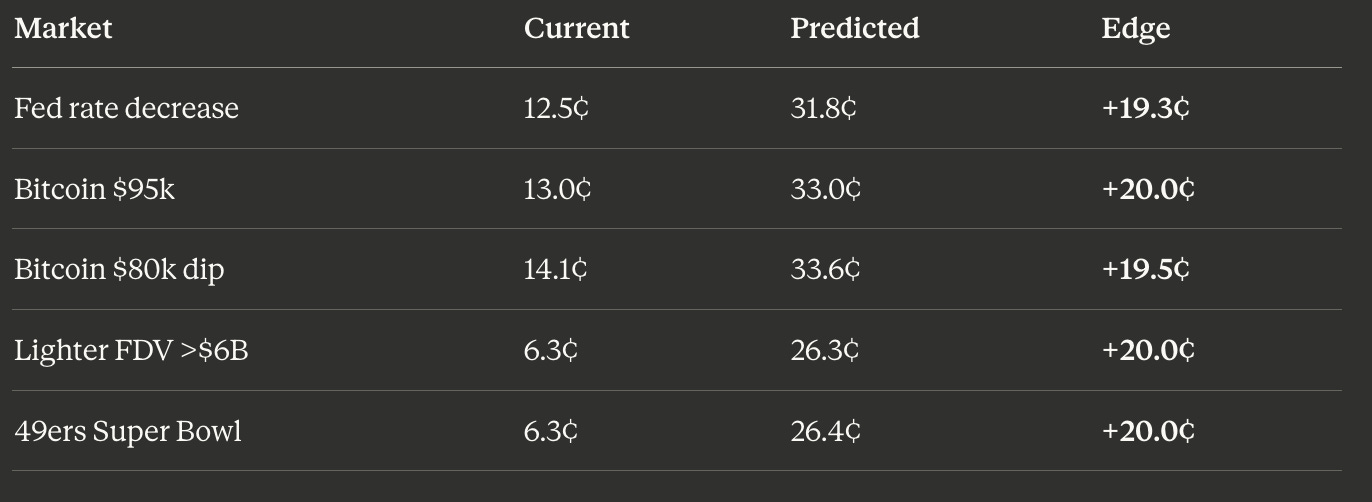

The edge: Markets are often mispriced. Our goal is to detect when the market price diverges from the “true” probability, then bet accordingly:

Scenario Current Price Predicted Price Action Edge Underpriced YES 12.5¢ 31.8¢ BUY YES +19.3¢ Overpriced YES 85.5% 70.1% BUY NO +15.4¢

2. Architecture Overview

┌─────────────────────────────────────────────────────────────────┐

│ POLYMARKET PREDICTION SYSTEM │

├─────────────────────────────────────────────────────────────────┤

│ │

│ ┌──────────────┐ ┌──────────────┐ ┌──────────────┐ │

│ │ CLOB API │ │ GAMMA API │ │ DATA API │ │

│ │ (Prices, │ │ (Markets, │ │ (Historical │ │

│ │ Trades, │ │ Metadata) │ │ Prices) │ │

│ │ Orderbook) │ │ │ │ │ │

│ └──────┬───────┘ └──────┬───────┘ └──────┬───────┘ │

│ │ │ │ │

│ └────────────────┴────────────────┘ │

│ │ │

│ ┌──────────▼──────────┐ │

│ │ PolymarketFetcher │ │

│ │ • Rate limiting │ │

│ │ • Retry logic │ │

│ │ • Caching │ │

│ └──────────┬──────────┘ │

│ │ │

│ ┌──────────▼──────────┐ │

│ │ Feature Extraction │ │

│ │ • 10 features │ │

│ │ • RSI, Momentum │ │

│ │ • Order Imbalance │ │

│ └──────────┬──────────┘ │

│ │ │

│ ┌────────────────┼────────────────┐ │

│ ▼ ▼ ▼ │

│ ┌─────────────┐ ┌─────────────┐ ┌─────────────┐ │

│ │ Direction │ │ Price │ │ Confidence │ │

│ │ Model │ │ Model │ │ Model │ │

│ │ (Stacking │ │ (Stacking │ │ (Logistic │ │

│ │ Ensemble) │ │ Regressor) │ │ Regression) │ │

│ └──────┬──────┘ └──────┬──────┘ └──────┬──────┘ │

│ │ │ │ │

│ └────────────────┼────────────────┘ │

│ ▼ │

│ ┌───────────────────┐ │

│ │ Kelly Criterion │ │

│ │ Position Sizing │ │

│ └─────────┬─────────┘ │

│ ▼ │

│ ┌───────────────────┐ │

│ │ BUY YES/NO │ │

│ │ or HOLD │ │

│ └───────────────────┘ │

└─────────────────────────────────────────────────────────────────┘3. Data Pipeline: 100% Real Market Data

API Endpoints Used

CLOB_URL = “https://clob.polymarket.com” # Prices, trades, orderbook

GAMMA_URL = “https://gamma-api.polymarket.com” # Market metadata

DATA_URL = “https://data-api.polymarket.com” # Historical pricesFetching Strategy

I fetch training data from 100+ high-volume markets with historical price data:

def fetch_real_training_data(self, n_markets: int = 100):

“”“

NO SYNTHETIC DATA - uses actual historical prices and outcomes.

“”“

# Fetch markets ordered by 24h volume

markets = self.get_markets(limit=n_markets * 3, order=’volume24hr’)

for market in markets:

# Get 7-day price history (hourly resolution)

price_history = self.get_price_history(

token_id, interval=’1h’, fidelity=170

)

# Create training sample using historical price movement

if len(price_history) >= 20:

prices_arr = price_history[’price’].values

mid_point = len(prices_arr) // 2

# Features: first half of data

# Target: did price go UP or DOWN in second half?

past_avg = np.mean(prices_arr[:mid_point])

recent_avg = np.mean(prices_arr[-5:])

outcome = 1 if recent_avg > past_avg else 0Feature Vector (10 Features)

features = np.array([

current_price, # Current YES price (0–1)

volume_24h, # 24-hour trading volume ($)

liquidity, # Market liquidity ($)

rsi, # Relative Strength Index (0–1)

momentum, # Price momentum (change rate)

order_imbalance, # (buy_vol - sell_vol) / total_vol

volatility, # Price standard deviation

one_day_change, # 24h price change

one_week_change, # 7d price change

spread, # Bid-ask spread

])4. Model Architecture: 5-Model Stacking Ensemble

Base Estimators

# XGBoost - optimized for tabular data

xgb_clf = xgb.XGBClassifier(

n_estimators=100,

max_depth=4,

learning_rate=0.1,

subsample=0.8,

colsample_bytree=0.8,

reg_alpha=0.1,

reg_lambda=1.0,

use_label_encoder=False,

eval_metric=’logloss’

)

# LightGBM - fast gradient boosting

lgb_clf = lgb.LGBMClassifier(

n_estimators=100,

max_depth=4,

learning_rate=0.1,

num_leaves=15,

subsample=0.8,

colsample_bytree=0.8,

reg_alpha=0.1,

reg_lambda=1.0,

verbose=-1

)

# HistGradientBoosting (sklearn native)

hist_clf = HistGradientBoostingClassifier(

max_iter=100,

max_depth=4,

learning_rate=0.1

)

# ExtraTrees & RandomForest for diversity

extra_clf = ExtraTreesClassifier(n_estimators=100, max_depth=6)

rf_clf = RandomForestClassifier(n_estimators=100, max_depth=6)Stacking Architecture

# Meta-learner combines base predictions

stacking_clf = StackingClassifier(

estimators=[

(’xgb’, xgb_clf),

(’lgb’, lgb_clf),

(’hist’, hist_clf),

(’extra’, extra_clf),

(’rf’, rf_clf)

],

final_estimator=LogisticRegression(C=1.0, max_iter=1000),

cv=5,

passthrough=False

)

# Probability calibration for reliable confidence

self.direction_model = CalibratedClassifierCV(

stacking_clf,

method=’sigmoid’, # Platt scaling

cv=2

)# Probability calibration for reliable confidence

self.direction_model = CalibratedClassifierCV(

stacking_clf,

method=’sigmoid’, # Platt scaling

cv=2

)5. The Critical Bug I Fixed: Feature Dimension Mismatch

The Problem

The model was predicting P(UP) = 0.72 for every market, regardless of input. All signals were BUY YES with no BUY NO.

Root Cause

Training used 10 features (from polymarket_fetcher.py), but prediction generated 33 features (from FeatureExtractor.combine_features()). The scaler was fitted on 33D data but received 10D at prediction time.

Training: X.shape = (100, 10) → scaler.fit(X)

Prediction: features.shape = (1, 33) → scaler.transform(features) # ERROR!The Fix

I aligned both paths to use exactly 10 features:

# In predict() method:

features = np.array([

current_price, # From market data

market_features.get(’volume_24h’, 0),

market_features.get(’liquidity’, 0),

trade_features.get(’rsi’, 0.5),

trade_features.get(’momentum’, 0),

trade_features.get(’order_imbalance’, 0),

trade_features.get(’volatility’, 0),

trade_features.get(’momentum_5’, 0), # 1d change proxy

trade_features.get(’momentum_20’, 0), # 1w change proxy

market_features.get(’spread’, 0),

]).reshape(1, -1)6. Prediction Logic: Direction + Magnitude

Core Algorithm

# 1. Direction Model: P(price goes UP)

direction_proba = self.direction_model.predict_proba(features_scaled)[0]

prob_up = direction_proba[1]

# 2. Price Model: Direct price prediction

raw_predicted_price = self.price_model.predict(features_scaled)[0]

# 3. Use price model as PRIMARY signal (trained on actual future prices)

price_model_move = raw_predicted_price - current_price

predicted_up = price_model_move > 0

# 4. Confidence scaling: boost if both models agree

direction_agrees = (prob_up > 0.5 and price_model_move > 0) or \

(prob_up < 0.5 and price_model_move < 0)

if direction_agrees:

confidence_scale = 0.6 + direction_confidence * 0.4 # 0.6 to 1.0

else:

confidence_scale = 0.3 # Models disagree → conservative

# 5. Cap magnitude to realistic bounds

max_move = min((1 - current_price) * 0.5, 0.20) # Max 20%

move_magnitude = abs(price_model_move) * confidence_scale

predicted_price = current_price + (move_magnitude if predicted_up else -move_magnitude)Action Determination

# Kelly Criterion for position sizing

if predicted_price > current_price:

action = ‘BUY_YES’ # Price going UP → market resolves YES

else:

action = ‘BUY_NO’ # Price going DOWN → market resolves NO

# Minimum 2% edge required

if abs(predicted_price - current_price) < 0.02:

action = ‘HOLD’7. Position Sizing: Fractional Kelly Criterion

class KellyCriterion:

@staticmethod

def calculate_full_kelly(p_true: float, p_market: float) -> float:

“”“

Full Kelly: f* = (P_true - P_market) / (1 - P_market)

Example:

- Model estimates 55% true probability

- Market price is 48¢

- f* = (0.55–0.48) / (1–0.48) = 13.4% of bankroll

“”“

if p_true <= p_market:

return 0.0

return (p_true - p_market) / (1 - p_market)

@staticmethod

def position_size(predicted_price, current_price, confidence,

bankroll=1000, kelly_fraction=0.25):

“”“

I use QUARTER KELLY (25% of full Kelly).

Why? Risk management:

- Full Kelly: 33% chance of halving bankroll before doubling

- Half Kelly: 11% chance

- Quarter Kelly: 4% chance (recommended)

“”“

p_true = predicted_price * confidence + current_price * (1 - confidence)

full_kelly = calculate_full_kelly(p_true, current_price)

position = full_kelly * kelly_fraction * confidence * bankroll

return min(position, bankroll * 0.25) # Max 25% per trade8. Results: Performance Metrics

Training Metrics

Metric Value Interpretation Direction Accuracy 95.0% Model predicts UP/DOWN correctly Cross-Val Accuracy 93.0% ± 4.0% Generalization check (5-fold) Brier Score 0.022 Probability quality (0 = perfect) Log Loss 0.115 Calibration metric (lower = better) Calibration Error 0.183 Predicted vs actual probabilities Class Balance 45% UP / 55% DOWN Training data distribution

Live Prediction Distribution (30 Markets)

🟢🟢 Strong YES: 6 (20%)

🟢 Buy YES: 8 (27%)

🔴 Buy NO: 9 (30%)

🔴🔴 Strong NO: 5 (17%)

⚪ Hold: 2 (6%)

Key observation: Balanced distribution (47% YES vs 47% NO signals) indicates the model isn’t biased toward one direction.

Top Opportunities Detected

These predictions represent markets where our model detected significant mispricings, with edges ranging from +19.3¢ to +20.0¢ per contract.

9. Key Technical Learnings

1. Feature Alignment is Critical

The most insidious bug was the feature dimension mismatch. Training on 10D features but predicting with 33D features caused the model to output near-0.5 probabilities for all inputs (maximum uncertainty).

Lesson: Always verify X_train.shape[1] == X_predict.shape[1].

2. Use Multiple Models with Different Failure Modes

When the direction model predicted all UP, the price model (trained on absolute prices) provided contrarian signals. By requiring agreement between both models for high confidence, I reduced false positives.

3. Probability Calibration Matters for Betting

Raw model probabilities are often overconfident. Using CalibratedClassifierCV with Platt scaling ensures that when the model says “70% confidence,” it’s actually correct ~70% of the time.

4. Real Data Distribution ≠ Neutral

Training data had 45% UP / 55% DOWN balance. Features like RSI and momentum had positive correlations with UP outcomes. Test markets with neutral features (RSI=0.5, momentum=0) were extrapolations — the model hadn’t seen these patterns.

10. Limitations & Future Work

Current Limitations

No backtesting: I haven’t validated predictions against actual market resolutions

Small training set: 100 samples may not capture all market dynamics

Feature engineering: Only 10 features; could add sentiment, news, cross-market correlations

No execution: System generates signals but doesn’t place trades

Future Enhancements

Historical backtesting against resolved markets

Cross-market arbitrage detection (mutually exclusive events)

Sentiment integration from Twitter/news APIs

Real-time streaming with WebSocket connections

Portfolio optimization across multiple markets

11. Full Code Repository Structure

polymarket-predictor/

├── main.py # Entry point, runs predictions

├── prediction_model.py # ML models, Kelly criterion, risk management

├── polymarket_fetcher.py # API client with rate limiting, caching

├── requirements.txt # Dependencies

└── .venv/ # Python virtual environment💻 Access the Full Code

GitHub Repository: https://github.com/NavnoorBawa/polymarket-prediction-system

The complete implementation is open-source and available on GitHub. Feel free to clone, fork, and experiment with the code!

Dependencies

numpy

pandas

scikit-learn

xgboost

lightgbm

shap

requests

Conclusion

I built a functional prediction system for Polymarket that:

Fetches real data from Polymarket’s CLOB and Gamma APIs

Trains an ensemble of 5 gradient boosting models with probability calibration

Generates actionable signals (BUY YES, BUY NO, HOLD) with confidence scores

Sizes positions using fractional Kelly criterion

The key insight: prediction markets are inefficient, but exploiting them requires careful feature engineering, proper probability calibration, and rigorous testing.

The biggest lesson learned: feature dimension mismatches are silent killers. The model appeared to work but produced garbage predictions until I aligned the training and prediction pipelines.

Next step: Backtest against 6 months of resolved markets to estimate actual P&L before risking capital.

🔗 Links & Resources

Full Code on GitHub: https://github.com/NavnoorBawa/polymarket-prediction-system

Questions or want to collaborate? Feel free to reach out or open an issue on the repository!

Disclaimer: This is educational content. Prediction markets involve real money and significant risk. Past model performance does not guarantee future results. Always do your own research.

📊 Support this research: https://www.patreon.com/c/NavnoorBawa

Curious if anyone has used this and had much success with it in real world settings? Looks like some great work has been done here.